Try it Now, Doc

Japan finally gets its jump start?

I’ve long argued that the market often tries to seek out whether intervention is likely. Given that 160 was the line in the sand for the MoF, traders were pushing for intervention. Well, last Tuesday, after a somewhat hawkish FOMC, the MoF decided to intervene in Dollar Yen as the pair drifted close to 161. It did so on Friday as well, and so it did this morning.

The message is clear: Tokyo wants to discourage speculation against the yen.

The background for Japan, however, has changed massively over the last six months, and one has to assess whether MoF intervention could be the nail in the coffin that finally makes the pair reverse course from here on out.

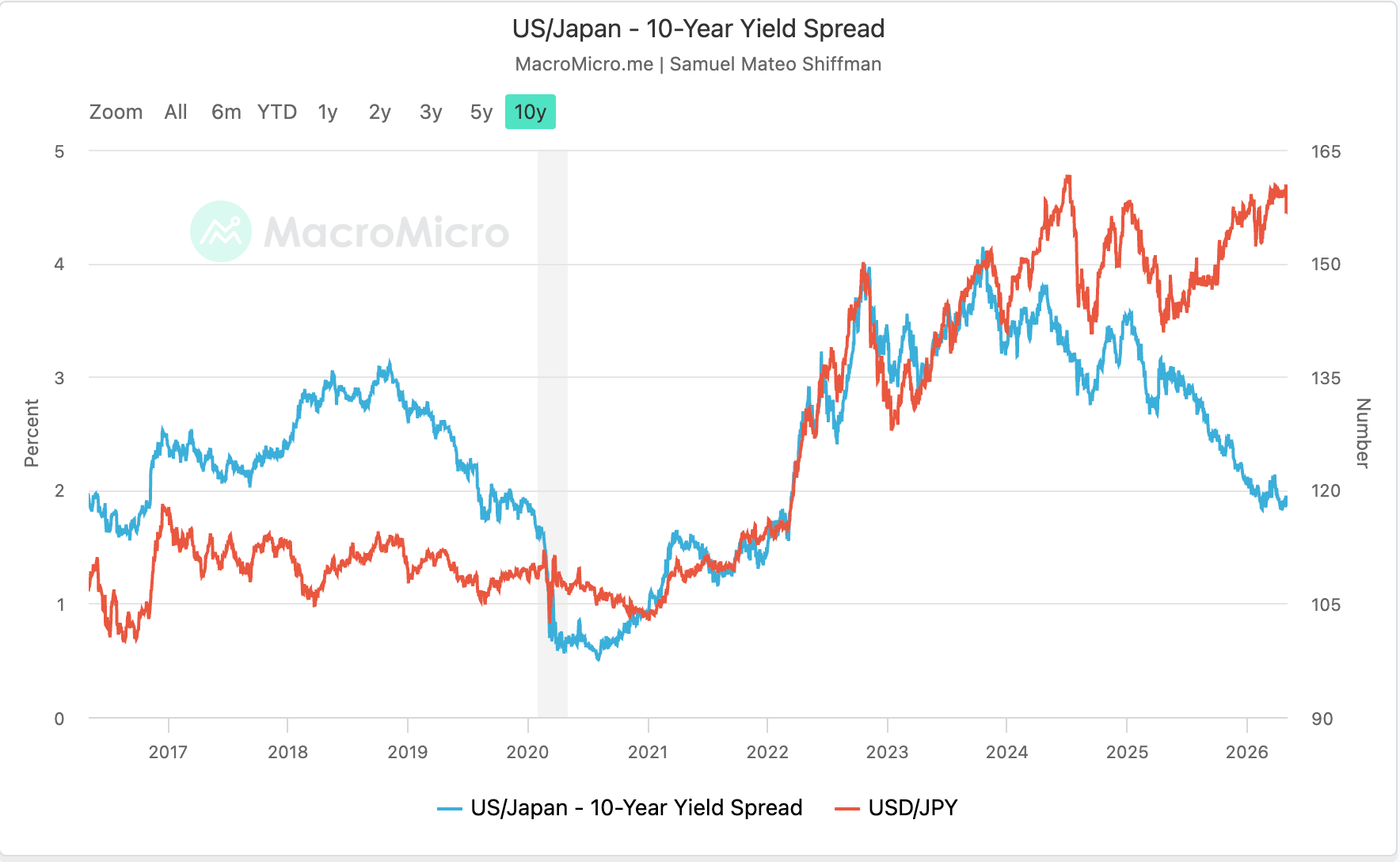

The reality is that Takaichi is pretty pro-market and pro-growth. In theory, she is the perfect candidate Japanese households and businesses need to finally revive the Japanese economy. Moreover, differential in US/Japan spread has narrowed big time favouring capital flows to come back to Japan.

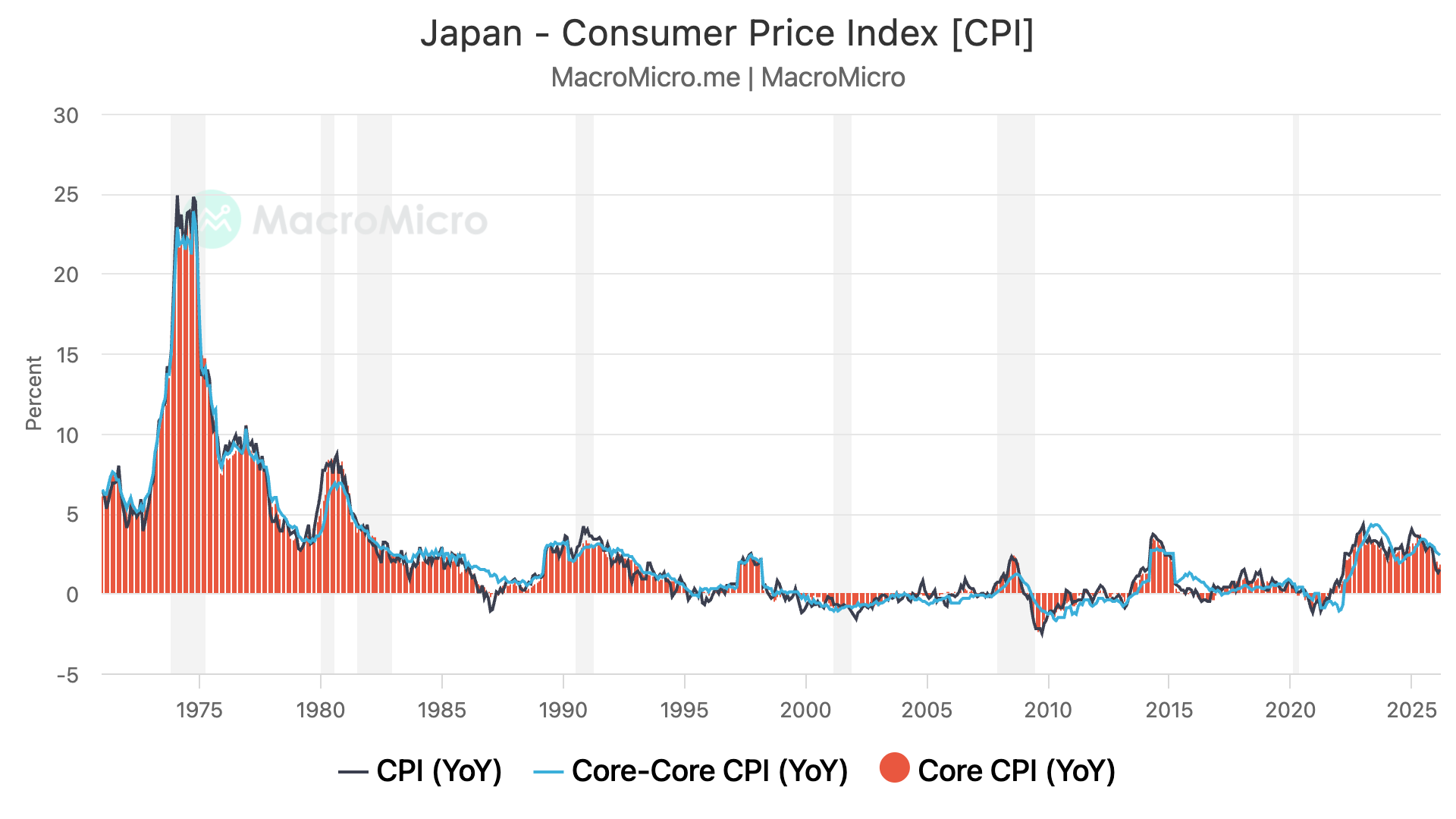

Inflation has finally reappeared in Japan, a phenomenon that had failed to happen sustainably for the last 20 years. The BoJ clearly wanted to see 2% inflation sustained in order to jump start the economy once and for all. Having G run above R for a sustained period should, in theory, help the case for its currency to slowly reprice higher.

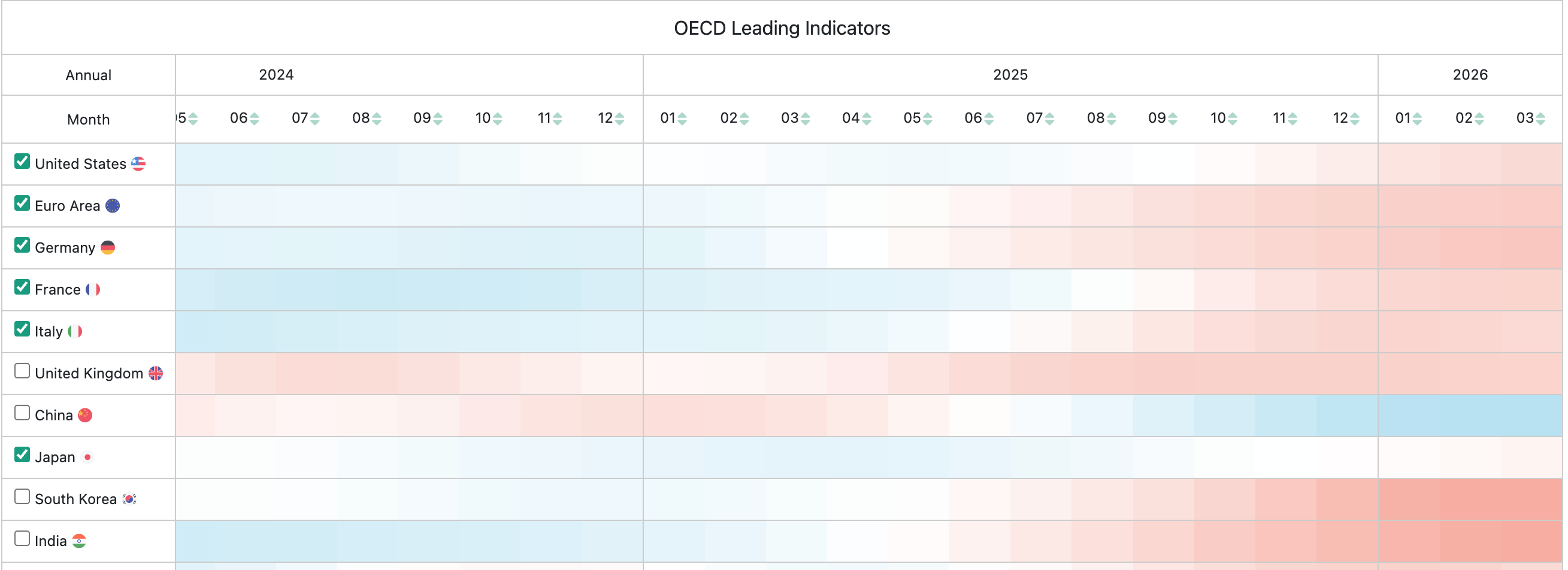

Looking at LEI, Japan appears to be joining its buddies in running it hot.

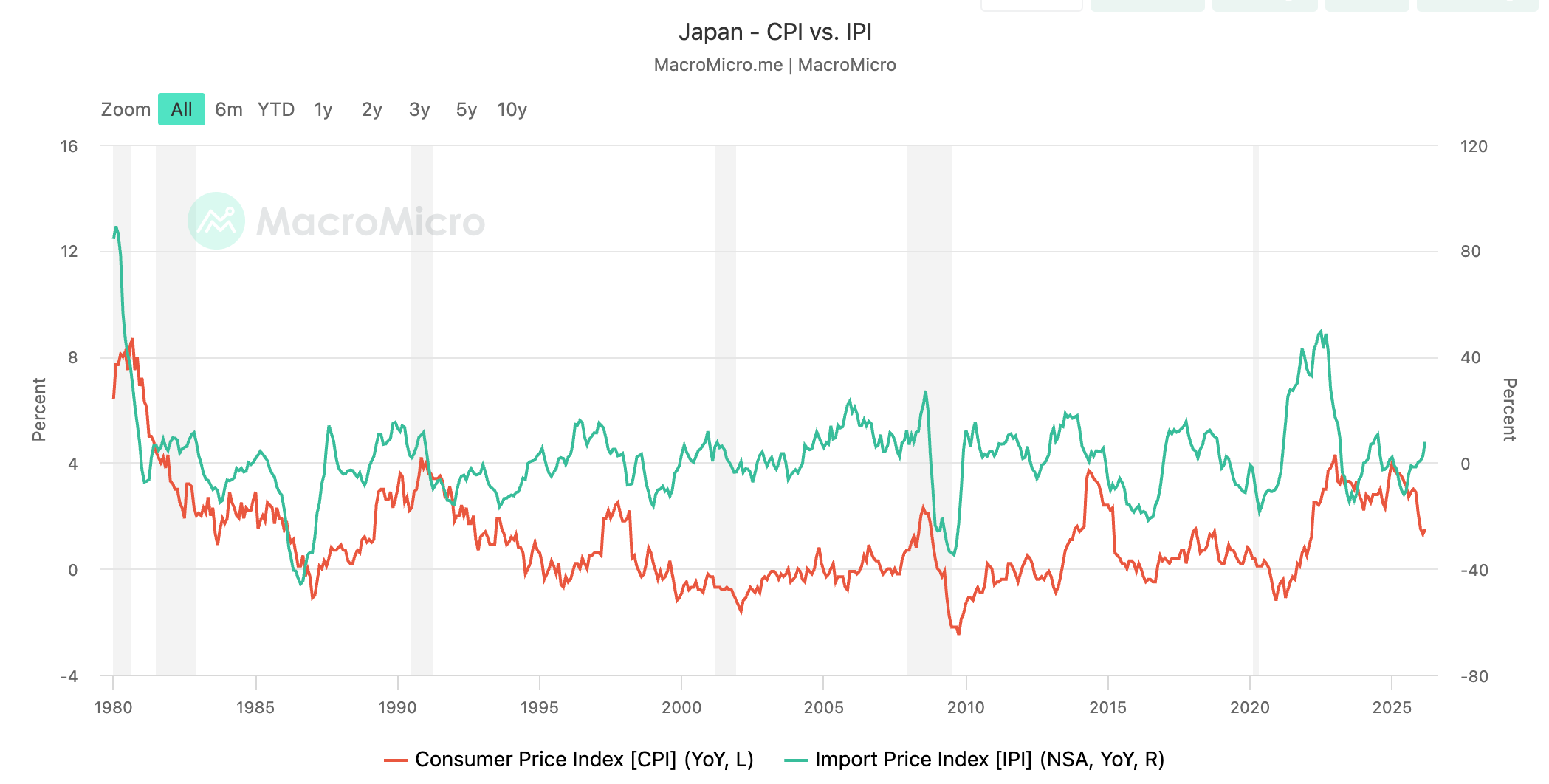

Japan is probably one of the most energy-sensitive countries there is. By allowing its currency to run this cheap, it is literally importing inflation via higher import prices. We saw this playbook during COVID, where most of the net inflation generated in Japan was due to supply-chain disruptions and a weak yen. The BoJ is probably, on one side, happy because this inflation shock is another jump start the economy needs to change household consumption and business investment patterns, which were lackluster for years. At the same time, the forward rate path for the BoJ is clearly up. It needed evidence that inflation was sustainably breaching 2%, it now has more than evidence, it has an entire playbook it has seen before.

Of course, long yen has been the widow-maker trade that almost every macro trader has tried at least once in their career. But a sustained geopolitical shock, combined with a more hawkish repricing of the BoJ and MoF intervention backstopping yen shorts, could finally allow the currency to reflect Japan’s changing macro backdrop.

The market remains stuck in the narrative that a yen revival is permanently out of reach. Yet Takaichi has already made history, and her political mandate gives her room to run the economy hot while addressing the deeper structural issues Japan has faced for decades. That combination may not be enough on its own, but the fact that both the BoJ and the MoF are joining in makes the yen story far more interesting than the market currently assumes.