Liquidity Conditions Are Deteriorating Rapidly: What's Next for Markets?

Correlation Breakdown Sends a Worrisome Signal

Friday’s price action was both telling and troubling. If the current correlation breakdown continues, we may be on the verge of a “COVID-like” response from central banks.

The dollar caught a strong bid late in the session, while gold and Treasuries sold off—a highly unusual combination. In a typical flight-to-safety environment, investors rotate into Treasuries, gold, the yen, and the Swiss franc as the safest corners of the market. But following Powell’s latest speech, the market seems to be signaling that the Fed is behind the curve and won’t be able to put a floor under this selloff.

At that point, sentiment shifted from safe-haven accumulation to an outright “dash for cash.”

Chart 1.a: When the dollar rallies while gold and Treasuries lose steam… something is broken.

Put simply: this was one of those “sell everything, just give me dollars” moments.

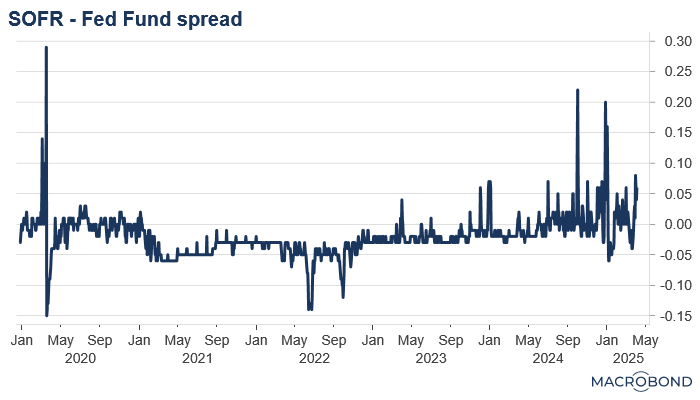

Liquidity Stress Is Escalating

The repo market—our proxy for dollar funding stress—is flashing warning signs. The cost of borrowing dollars while simultaneously lending against dollar collateral is rising fast. The triparty repo rate has broken above the RRP rate, and the SOFR–Fed Funds spread is widening. These are classic signs of deteriorating liquidity conditions.

And they’re accelerating.

Chart 1.b: Watch out, funding markets are worriesome

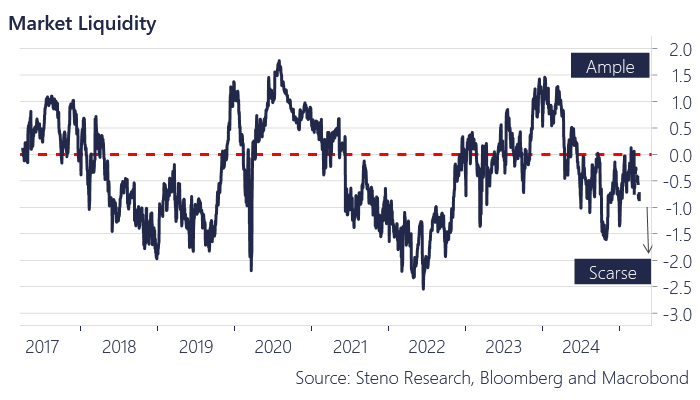

When we combine signals from bond market volatility, collateral value, dollar strength, and Fed liquidity—as a proxy for overall market liquidity—we see clear evidence that dollars are becoming scarce.

Chart 1.c: Market liquidity is becoming scarse

This tightening is showing up in the macro curve as well. Both the 5y5y inflation swap rate and the term premium have rolled over sharply. Earlier in the cycle, rising term premia reflected concern about persistent fiscal expansion and elevated Treasury issuance. Now, the synchronized decline points to waning inflation fears and a renewed focus on tightening liquidity and shrinking fiscal momentum.

Chart 1.c: Inflation looks to be contianed, and Term Premia too

In short, the market is no longer worried about long-term deficit pressure—it’s worried about immediate access to cash. This repricing compresses the term premium, reflecting both falling inflation expectations and diminished belief that fiscal policy will continue to exert upward pressure on yields.

We’re clearly shifting from a reflationary narrative to one driven by liquidity concerns.

If term premia continue to decelarate, Fiscal options are back on the table & Bessant will give Trump the green light.

Chart 2.a: Even as deficit continues to expand, term premia is going lower. That’s a healthy sign. Market can absorb more debt.

What Would a “COVID-Like” Fed Response Look Like?

If funding conditions continue to deteriorate at this pace, something in the bond market may snap.

In early 2020, amid peak bearishness, the Fed called an emergency meeting and unleashed a barrage of monetary support. The result was one of the fastest V-shaped recoveries in equities and a strong bid for fixed income.

Keep reading with a 7-day free trial

Subscribe to Clark Street to keep reading this post and get 7 days of free access to the full post archives.