Exorbitant Privilege: Inside the Mechanics of Dollar-Based Hegemony

And Why April 2nd, 2025, May Be Remembered Not as the Day of Liberation, but the Moment the Empire Lost Its Grip.

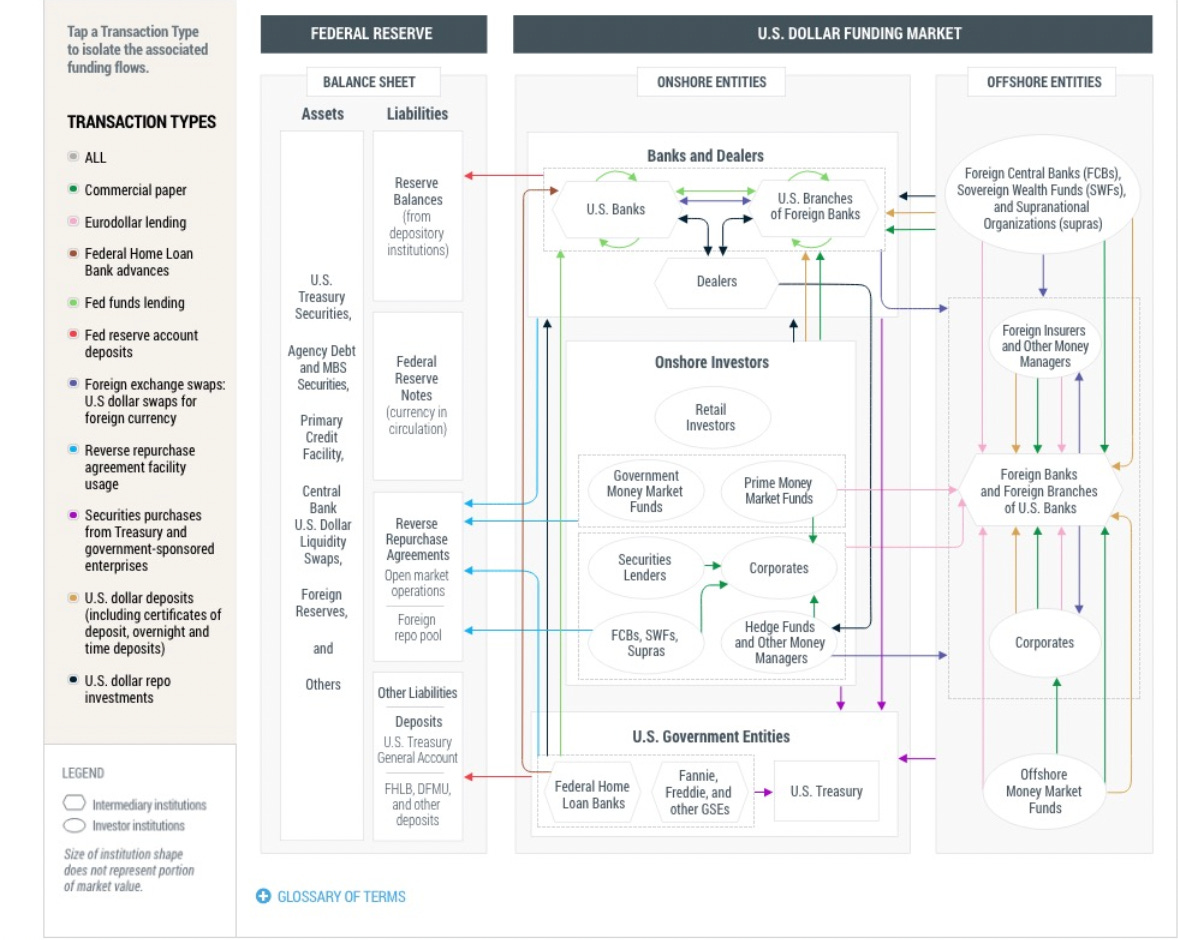

Dollar Liquidity in the Traditional Regime

USD as Global Reserve and Collateral

The U.S. dollar has long sat at the core of the international monetary system, serving as the global reserve currency and the backbone of cross-border finance. Dollar-denominated assets – especially U.S. Treasury securities – are widely held as reserves by central banks and used as safe collateral in financial markets worldwide. This reserve role means the dollar system extends far beyond U.S. shores. In fact, an enormous offshore USD ecosystem (the Eurodollar market) allows banks outside the U.S. to create dollar loans and deposits without direct Federal Reserve oversight. Through this offshore dollar credit, and via the shadow banking system, the dollar provides the bedrock collateral for global lending. For example, U.S. Treasuries can be re-used (rehypothecated) in repo and derivative markets to back new loans, multiplying dollar liquidity throughout the world. In sum, the dollar’s status as universal collateral and unit of account underpins its outsized influence on global funding conditions.

The Dollar Liquidity Transmission Mechanism

Chart 1.a: Base liquidity from the Fed and onshore USD markets feeds into offshore dollar lending and back, transmitting liquidity worldwide.

At the heart of the dollar-based regime is a liquidity transmission mechanism that links central bank money to broader credit growth. The Federal Reserve (and other central banks supplying USD liquidity) traditionally influences credit by expanding or contracting base money (bank reserves and currency). In the modern system, however, liquidity flows less through simple deposit multipliers and more through wholesale funding markets. For instance, when the Fed injects funds via repo operations (buying Treasuries from dealers in exchange for cash), it directly increases money-market liquidity. Banks and dealers then reuse that cash to lever up – purchasing more bonds or making loans, often using those bonds as collateral to borrow yet more. This sets off a chain reaction: rising liquidity pushes up asset prices and collateral values, which in turn encourages additional borrowing against those now more valuable assets. Through such channels, dollar liquidity moves from the central bank’s balance sheet into global credit expansion and asset markets.

This “plumbing” enables the dollar to lubricate global finance, but it also means stress can transmit quickly. A shortage of bank reserves or Treasuries, for example, can constrain repo funding and reverberate through the entire chain, tightening credit. Conversely, abundant reserves and collateral can lead to rapid credit creation. The dollar liquidity engine thus relies on confidence and continuous flow through these channels.

Strong vs. Weak Dollar: Effects on Global Credit Cycles

Because of the dollar’s central role, its value (exchange rate) tends to correlate inversely with global risk appetite and credit growth. In the “old world” pattern, a strong dollar often accompanies or causes tighter financial conditions globally. When the dollar appreciates strongly, it effectively raises the debt burden on borrowers outside the U.S. (who often have USD liabilities) and can induce capital outflows from emerging markets. Historically, a surging dollar has been associated with stress in dollar funding markets – liquidity becomes scarce worldwide, cross-border credit shrinks, and investors turn risk-averse. Empirically, during such periods sensitive international asset prices plunge and credit spreads widen, while cross-border lending and leverage retrench sharply. In other words, a strong dollar tends to compress global credit creation and dampen risk-taking.

By contrast, a weak dollar usually signals easier global liquidity and greater risk appetite. When the dollar falls, foreign currencies strengthen, reducing pressure on overseas borrowers and encouraging capital to flow into riskier markets. A cheaper dollar often correlates with rising commodity prices and better financing conditions in emerging economies. This dynamic was seen in past dollar down-cycles that spurred “reflation” trades – capital flooded into stocks, EM credit, and other risk assets as global dollar funding became more abundant. In essence, a weak dollar has functioned as a relief valve that boosts global credit growth and investment, whereas a strong dollar acts as a cap on those activities. This inverse relationship between the dollar’s value and global risk conditions was a core feedback loop in the traditional regime.

The Global Liquidity Hierarchy and Pools

Michael J. Howell, in Capital Wars, describes global liquidity as a hierarchy or layered pool of funding, rather than a single monolithic quantity. At the base of this hierarchy is high-powered money – the narrowest liquidity consisting of central bank reserves and currency. But crucially, Howell expands the base to include a “shadow monetary base” of offshore dollar wholesale markets and available collateral. In other words, the foundation of global liquidity includes not just central bank money, but also the Eurodollar deposits and repo-able safe assets that function like base money for private markets. Stacked atop this base is a much larger tower of private-sector credit. Banks, shadow banks, and capital markets create broad liquidity (loans, bonds, etc.) by leveraging that base via credit and money market instruments.

Howell identifies three major global liquidity pools: (1) Private sector funding (e.g. bank lending, shadow bank credit), (2) Official liquidity (central bank balance sheets and policy liquidity), and (3) Cross-border flows (foreign lending and investment across borders). These pools interact in complex ways. For instance, an emerging-market corporate might receive a dollar loan (private liquidity) that was funded by a European bank tapping the Eurodollar market (cross-border liquidity), which in turn may have been enabled by the European Central Bank’s easy policy (official liquidity). The liquidity hierarchy is often visualized as an inverted: a small base of hard liquidity supports a much larger volume of credit on top. If the base (reserves + collateral) expands, it can support a larger credit superstructure – akin to widening the foundation of a pyramid. If it contracts or becomes unstable, the broader liquidity pyramid can wobble or shrink (as in a credit crunch). This hierarchical view underscores why safe assets and central bank reserves are so critical: they are the anchor of the entire global credit edifice.

Chart 1.a: Michael Howell’s Liquidity Hierarchy

Divergence in the Current Macro Regime

Over the past couple of years, macroeconomic conditions have been unfolding in a way that diverges from those traditional patterns. We are witnessing scenarios that “break” the usual feedback loops of the dollar system. Most notably, the U.S. dollar has been weakening even as U.S. interest rates and yields climb, a combination that historically has been rare. This has profound implications for global liquidity and credit.

A Weaker Dollar Amid Rising Yields: An Unusual Combination

U.S. Treasury yields surged to near multi-year highs while the U.S. dollar has simultaneously declined. Typically, one would expect higher U.S. yields (if driven by Fed tightening or strong growth) to attract capital and strengthen the dollar. Instead, the opposite happened – a dynamic that former Fed Chair Janet Yellen called “a very unusual pattern”. Investors did not flock to Treasuries as a safe haven despite market turmoil; rather, Treasury prices fell (yields up) and the dollar fell too. Normally in uncertain times, global investors seek safety in U.S. assets (boosting the dollar since Treasuries are dollar-denominated), but recently Treasury yields have skyrocketed and the dollar has declined, suggesting investors are beginning to shun dollar-based assets and even questioning the safety of U.S. Treasuries.

In other words, rising yields in this episode are not a signal of confidence or attractiveness, but of reduced demand for U.S. bonds. The usual inverse correlation between yields and the dollar has flipped. Global investors seem to be reassessing the quality and safety of U.S. debt in a more fragile, multipolar global environment. This shift can be seen as a feedback loop breakdown. In the past, if U.S. yields rose sharply, the dollar often strengthened (tighter U.S. policy would drain global liquidity and entice capital into dollar assets). Now, rising yields are being accompanied by capital outflows or at least lackluster inflows, putting downward pressure on the dollar. The result is a weaker dollar even as U.S. interest rate differentials widen in theory.

What might explain this puzzling divergence? A few factors stand out.

First, concerns about U.S. fiscal sustainability and inflation have grown. With U.S. public debt swelling and inflation pressures lingering, some investors fear that high yields reflect credit and inflation risk rather than just a temporarily strong economy. This erodes the “safe haven” allure of Treasuries.

Second, global geopolitics and trade tensions (for example, the re-emergence of tariffs or sanctions) have made some countries less eager to hold U.S. assets. If foreign official players are not buying Treasuries like before (or are even selling), higher yields no longer translate to dollar strength. In fact, 2024 saw foreign central banks as net sellers of U.S. government debt – the official sector offloaded roughly $60 billion of Treasuries over the year.

Third, market technicals and volatility have played a role. Rapid swings (volatility) in rates and currency markets can lead to feedback loops where the usual correlations break down. Citriniti points out that we are in a regime of elevated macro volatility and shifting central bank actions, which is undermining the old relationships between currencies and yields. Investors are repositioning faster and more defensively, sometimes treating the dollar and U.S. bonds both as things to avoid (a stark contrast to the old “sell stocks, buy dollars and bonds” playbook).

The significance of this shift is hard to overstate. It signals a potential loss of confidence in the U.S. dollar’s unique status. Such a pattern is a departure from the typical risk-on/risk-off cycles of the past and indicates that investors are seeking alternatives outside of the dollar-based assets altogether.

Broken Feedback Loops and Global Liquidity Implications

In the traditional regime, there were self-correcting feedback loops. For instance, if U.S. yields rose, the stronger dollar and higher borrowing costs would eventually tighten global liquidity, dampening growth and causing yields to fall back as demand for safe assets returned. Now, those mechanisms seem impaired. The dollar weakening alongside rising U.S. yields eases one traditional constraint (a weaker dollar should be positive for global liquidity), but it also suggests something more pernicious: liquidity is not returning to U.S. markets as before. If global investors aren’t stepping in to buy Treasuries, who will fund U.S. deficits at reasonable rates? The answer has been domestic buyers at higher yields, which pulls cash out of other uses.

From a global liquidity standpoint, this situation is murky. On one hand, a weaker dollar usually loosens financial conditions abroad – it can boost commodity prices and EM financing, as discussed. On the other hand, if the cause of dollar weakness is eroding confidence in dollar assets, that can tighten global liquidity in other ways (e.g. through higher risk premiums). We may be seeing a fragmentation: liquidity is not flowing uniformly. Some traditional dollar liquidity might even be leaking out of the U.S. system and finding other channels (for example, into gold, into non-dollar assets, or simply staying on the sidelines).

Chart 1.c: Rising Risk Premia is a symptom of eroding confidence in dollar assets

Citriniti’s emphasizes how changes in capital flows and central bank behavior are altering the narrative. One change is the role of foreign central banks and sovereign investors. In the past, they were big providers of global liquidity by recycling dollar trade surpluses into U.S. bonds (the classic “petrodollar” and Asian surplus recycling). Now, many of these actors are diversifying reserves and reallocating flows. Recent data show the dollar’s share of global FX reserves has dropped to roughly 57%, the lowest in decades, as central banks actively reduce USD holdings and increase gold and alternative currencies.

Chart 1.d: USD % of Total Reserves Are Slowly Heading Lower

This means less automatic support for U.S. asset prices and a potential structural weakening of one source of global dollar liquidity. Central banks in emerging markets, for example, might intervene less to support their currencies (since a weaker dollar reduces pressure on them) and therefore accumulate fewer dollar reserves. Collectively, these shifts break the old loop where capital out of the rest of world reliably flowed back into U.S. dollar assets during times of stress.

Another broken feedback loop relates to the interest rate differentials. Normally, wide rate gaps draw arbitrage – if U.S. yields far exceed those in Europe or Japan, investors there would borrow cheaply in euros or yen to buy higher-yielding USD assets, which supports the dollar. However, the FX swap basis (the cost to swap other currencies into dollars) has at times been elevated, eating away the arbitrage gains. Episodes of USD funding stress have made it costly or risky to do these trades, meaning rate differentials don’t translate into capital inflows as smoothly.

Chart 1.e: Cross Currency Basis Swap are volatile

Additionally, yield gaps are narrowing from the other side: other major central banks (ECB, BoJ) are also stepping back from easy money. The Bank of Japan, for instance, has begun allowing its yields to rise (tweaking yield-curve-control policy). This reduces the incentive for Japanese investors to seek yield abroad – some Japanese funds have even sold U.S. bonds to move money back home as domestic yields became more attractive. That is new: in prior eras, Japanese and European institutional investors were dependably thirsty for higher-yielding dollar assets when their local rates were zero. Now with global rates up and synchronized tightening (or less easing), those flows are diminished. The feedback loop where “lower foreign yields => more dollar buying” is not as strong, since foreign yields aren’t so low anymore.

Chart 1.f: Domestic Yields are now attractive, making U.S bonds less attractive internationally

The net effect on global liquidity is a bit paradoxical. Global dollar liquidity (the availability of dollar funding worldwide) might improve from a weaker dollar in some respects – for example, countries that were strained by a strong USD get breathing room, possibly reducing their need to tighten policy or liquidate assets. However, if U.S. financial conditions are tightening (due to higher yields and the continuation of QT (pace slower, but timeline longer) without the offset of foreign inflows, overall global financial conditions can still be restrictive.

We are witnessing pockets of easing (like China injecting liquidity to counter its slowdown) but also pockets of stress (like rising default risk in parts of the world). TGA drawdown, than refilling (april), than continuation… Thus, the usual smooth global liquidity tide that lifted when the dollar fell is less uniform now. The old regime’s cause-effect chain (Fed policy → dollar value → global liquidity) has splintered into multiple pathways.

Is Ex-US Credit Benefiting from the Dollar’s Weakness?

A key question in this divergence is whether the rest of the world is actually benefiting from the weaker dollar, as they normally would. In theory, a softer dollar should reduce foreign financing costs, boost commodity prices (helping exporters), and encourage international credit growth. Despite the dollar’s pullback, several factors are constraining ex-U.S. credit.

One major factor is rising real interest rates. While the dollar’s nominal value fell, U.S. real yields shot up to multi-year highs. This reflects a higher global cost of capital. Many foreign borrowing rates are benchmarked to U.S. yields or influenced by them. So, emerging market corporates might find that even though their local currency strengthened a bit, the base interest rate they pay on new dollar loans is much higher than a year or two ago. High real rates globally are a headwind for new credit formation – they make loans less affordable and investment projects less attractive.

Chart 1.g: Real Yields are expensive. Making credit formation less likely

Another constraint is the ongoing trend of geopolitical realignment and caution. Global banks and investors are more choosy now in allocating credit across borders, due to geopolitical risks. For instance, U.S.-China financial/trade decoupling has meant less U.S. bank lending and less portfolio investment flowing into China – a stark change from the 2000s when a weak dollar would spur huge EM inflows. Also, if global trade slows down, the need to settle (demand) in USD diminishes. Similarly, Western sanctions on Russia and concerns about potential future sanctions have made some institutions reduce exposures. So, even though the dollar is weaker, not all regions are equally benefiting – some are effectively walled off or viewed with caution, limiting their credit boom. Meanwhile, U.S. credit demand (government in particular) is dominating capital markets with heavy Treasury issuance, which can crowd out some lending to riskier overseas borrowers.

Citriniti observes that simply having a weaker dollar is not a panacea for ex-U.S. borrowers in the current environment. He notes that why the dollar is weakening matters: if it’s due to a benign cycle (U.S. easing policy, improving global growth), then yes, ex-U.S. credit typically jumps. But if the dollar is weakening because of U.S. structural issues and a reordering of global finance, the benefit can be nullified by risk aversion and fragmentation.

There is also an element of “once bitten, twice shy”: the violent dollar surge in 2022 that caused a global dollar shortage is fresh in memory, so borrowers and lenders remain conservative, fearing that conditions can change again. This has led to ex-U.S. credit markets being slow to trust the recent dollar weakness as durable. In effect, the rest of the world is saying: “We’ll believe the dollar is truly tamed when we see it.” Until then, credit expansion remains cautious.

Shifting Flows and Policy Regime Changes

Another aspect of the current divergence is the re-routing of financial flows and policy priorities around the world. We touched on foreign central banks reducing their U.S. Treasury purchases. This trend can be seen as part of a broader “de-dollarization” impulse, where countries seek to reduce reliance on the dollar-centric system. This doesn’t mean an abrupt end to dollar use, but it has led to incremental changes: more bilateral trade in local currencies, more gold accumulation by central banks (global central bank gold purchases hit record levels recently), and the exploration of alternative payment systems. For instance, according to Bank of America, central banks’ gold purchases exceeded 1,000 tons for three consecutive years (2022–2024), and the dollar’s share in reserves fell by over 8 percentage points in the last decade. These shifts indicate that foreign reserve strategy is actively moving away from an all-dollar diet. The immediate impact is that one classic source of global dollar demand (official FX reserve growth) is weaker, which can contribute to a softer dollar and also means less recycled liquidity into U.S. markets.

Additionally, central bank policy divergence has come into play.

One notable regime change is the Bank of Japan’s policy shift. The BoJ for years kept 10-year yields near 0%, driving Japanese investors overseas in search of yield (a big support for global bonds). In late 2023, the BoJ raised the cap on yields (allowing 10-year JGB yields up toward 1%). This led to a reversal of some flows: Japanese insurers and funds began hedging less or selling some foreign bonds to take advantage of higher domestic yields. The U.S. felt this as reduced demand for Treasuries at the margin. It is a reversal of a decades-long dynamic, and it contributed to the rise in U.S. yields without dollar support. Essentially, one pillar of the old dollar-liquidity regime – Japan as a steady dollar buyer – became less reliable.

Citriniti emphasizes that these shifting flows – whether it’s central banks diversifying, or private investors reallocating due to new risk perceptions – are creating a more volatile and less USD-centric macro environment.

In the current divergence regime, we also see higher macro volatility – partly due to these inconsistent flows and policy cross-currents. One outcome has been more frequent surprises (e.g. abrupt moves in currency values or bond yields) that catch markets off guard. The narrative among investors is shifting to acknowledge that the old heuristics (like “Don’t fight the Fed” or “weak dollar = buy EM”) may not hold without nuance.

Trump Agenda’s: Can we take this admnistration seriously.

One could argue that the stability of the bond market was already fragile, and most of the above trends were working slowly in the background. The trump administration simply pressed on the accelerator.

I do think it’s very possible, say in 50 years, that we picture April 2nd 2025 not as the day america “liberated itself”, but as the day america saw the fall of it’s exorbitant privilege and with that, it’s overaching influence on the world.

When does a company declare bankruptcy, one could ask? Well, bad decisions. And when it comes to America, its unique competitive advantage “is—or was—its ability to issue predominantly “safe” assets in the form of U.S. currency and Treasuries, which are—or were—in high demand by foreign official and private sectors, and to use the proceeds to fund riskier international assets: equities, foreign bonds, and direct investment in overseas businesses.” In essence, the U.S. ran the ultimate carry trade—exporting paper, importing returns.

But when the world starts questioning the “safety” of those assets, and the demand for Treasuries becomes conditional or reluctant, the spread narrows, the privilege erodes, and what once looked like a free profit begins to resemble a leveraged position with rising funding costs and evaporating margin. And just like any company that borrows short to invest long, the turning point comes not when the balance sheet says so, but when confidence disappears.

This chart is not just about numbers—it’s a diagnostic of how U.S. financial hegemony works, and how close we may be to testing its structural limits. The widening gap is the cost of sustaining that privilege. The risk now is whether the world continues to fund it.

America’s Global Carry Trade: The Widening Gap Between U.S. Foreign Assets and Liabilities

Unto Trading...

Liquidity conditions are becoming increasingly scarce, and the usual playbook—where a weaker dollar supports global liquidity—isn’t working this time. The system is strained. One way or another, the Fed will likely be forced into monetizing U.S. debt again, becoming the marginal buyer of Treasuries.

Keep reading with a 7-day free trial

Subscribe to Clark Street to keep reading this post and get 7 days of free access to the full post archives.